Global Mortgage Group Steps Up as Singapore’s Bank Lending slowdown fuels demand for bridging loans and private credit

The Perfect Storm for Bridging Finance

In some of the world’s most sophisticated property markets — Singapore, the United States, London, Australia, and Canada — a unique set of market forces is creating a surge in demand for bridging loans.

High net worth investors in these regions are sitting on unprecedented levels of built-up property equity. At the same time, traditional bank lending has slowed sharply, driven by stricter credit policies, higher interest rate environments, and longer approval timelines. This gap between capital locked in assets and the need for liquidity is where bridging loans shine.

Why Bridging Loans Are in Demand

Bridging loans are short-term, asset-backed financing tools designed to “bridge” liquidity needs until longer-term funding or asset sales are completed. For HNW investors, they provide speed, flexibility, and discretion — qualities increasingly absent from conventional bank lending.

Key Drivers Across These Markets:

How Bridging Loans Work for the Ultra-High-Net-Worth

Bridging loans allow property owners to extract equity quickly, often in weeks rather than months, for purposes such as:

Why This Matters for Private Bankers & Advisors

For client advisors and private bankers, understanding bridging finance is essential in the current market. Clients with significant real estate portfolios often face moments when timing is critical, but traditional financing lags behind. Bridging loans offer a way to:

How Global Mortgage Group Fills the Gap

At Global Mortgage Group (GMG), we specialize in unlocking global property wealth. Our bridging loan solutions are designed for high net worth individuals and families who need fast, discreet, and flexible access to capital across multiple jurisdictions.

GMG offers:

With GMG, your property’s equity becomes a powerful, accessible asset—ready to deploy wherever opportunity arises.

Refer a Client => Earn a Fee

We also reward our professional network. Global Mortgage Group pays a generous referral fee for introductions that lead to successful bridging loan transactions. Whether you are a client advisor, private banker, lawyer, or accountant, partnering with GMG can add immediate value to your client relationships—and your bottom line.

An Era of Equity Liquidity

As wealth concentration in prime real estate continues, and with conventional banks becoming more restrictive, bridging finance is evolving from a niche product into a mainstream strategic tool for sophisticated investors. For HNW individuals in Singapore, the U.S., London, Australia, and Canada, it’s not just about borrowing — it’s about unlocking dormant capital to stay agile in a competitive global investment landscape.

Please contact me directly if you would like to learn more about our global bridging loan options.

Your Top Questions Answered:

1: What is driving the growing demand for bridging loans in global property markets?

Stricter bank lending, longer approval times, and rising equity levels are pushing investors toward bridging loans for fast and flexible financing.

2: How do bridging loans benefit high net worth investors?

They provide rapid access to capital for acquisitions, refinancing, equity release, or seizing time-sensitive investment opportunities without forced asset sales.

3: Why are bridging loans considered more flexible than traditional bank lending?

They are asset-backed, processed quickly, and structured creatively to meet complex ownership needs, unlike conventional loans burdened by compliance delays.

4: How does Global Mortgage Group support clients with bridging finance?

GMG offers cross-border expertise, rapid execution, and access to a wide global lender network, ensuring discreet and tailored financing solutions for wealthy investors.

5: Can professionals benefit from referring clients to GMG for bridging loans?

Yes, GMG pays referral fees to advisors, bankers, lawyers, and accountants who introduce clients, creating added value for both professionals and their clients.

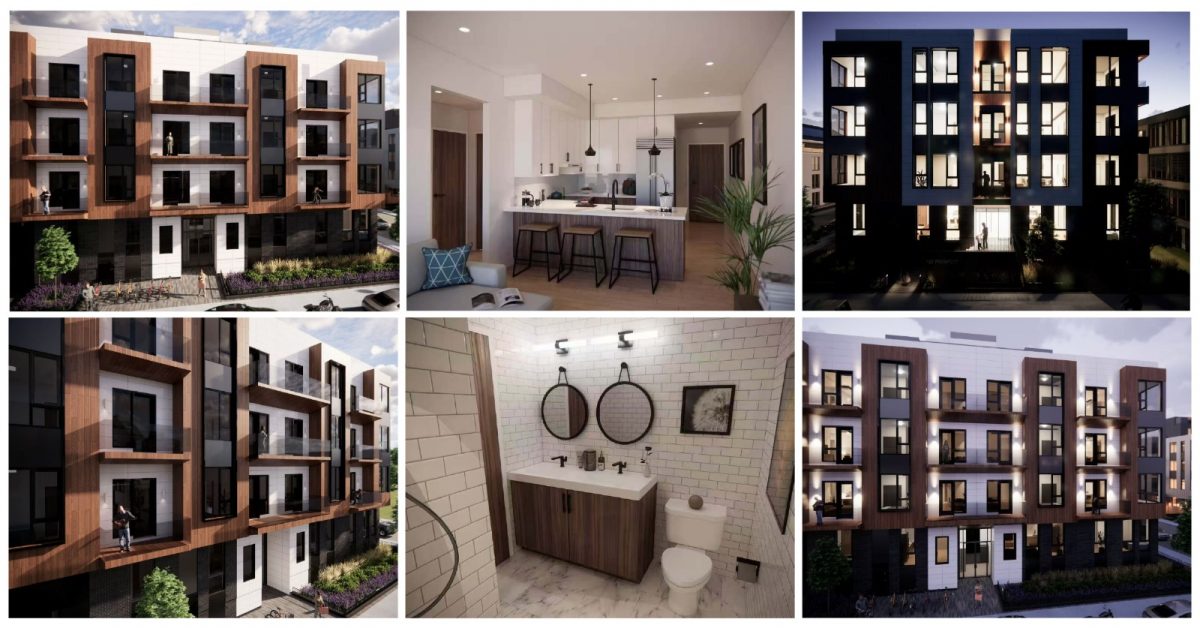

Act Fast: Rare New Boston Condos Hitting the Market Now

There are missed opportunities. And then there’s missing out on the only new condo development in Cambridge, Boston, right next to Harvard and MIT. For global investors, this isn’t just another property launch. It’s a rare chance to own real estate in one of the most competitive and tightly held markets in the U.S.

Why This Is a Rare Opportunity

Secure a Home Near Boston’s Best Schools

Boston is one of the most sought-after cities in the world for education. With prestigious schools, colleges, and universities in every direction, owning a home here is a smart move for families with children who may eventually study in the U.S.

Financing Available for Overseas Investors

Investors can access financing options for U.S. property purchases through our subsidiary America Mortgages. Financing is available to foreign nationals and U.S. expats. No U.S. credit score or income is required. You can even refinance or cash out from an existing U.S. property to fund this purchase.

About the Property

A boutique project with only 13 units remaining (total of 26), ranging from 570 to over 1,000 square feet. Unit types include studios, one-bedroom, two-bedroom, and three-bedroom layouts.

Prices range from $700,000 to $1.5 million.

All units feature modern designer interiors and are optimized for high rental appeal.

Cambridge isn’t just a great neighborhood. It’s a protected ecosystem with world-class demand, virtually no supply, and one of the most educated and affluent renter populations in the country. This property is the only new build in the area. Once it's gone, there may not be another chance like it for years.

Perfect for investors, ideal for families. This is a smart move any way you look at it.

Ready to learn more? Email, WhatsApp, or schedule a call with me directly.

Your Top Questions Answered:

Q1: Why are these new Boston condos considered a rare investment opportunity?

A: Cambridge has extremely limited new developments due to strict zoning and preservation rules, making this the only new condo project near Harvard, MIT, and Kendall Square.

Q2: What makes the location in Inman Square so desirable?

A: Inman Square offers a walk able, vibrant lifestyle surrounded by restaurants, boutiques, and research centers. Its proximity to Harvard and MIT ensures lasting rental demand.

Q3: Are these condos suitable for rental income or personal use?

A: Yes, the condos deliver 5 to 6 percent average rental yields with strong tenant demand, while also being perfect for families wanting a long-term home near Boston’s top schools.

Q4: Can international buyers get financing for these Boston condos?

A: Yes, overseas investors can access financing through America Mortgages, a subsidiary of Global Mortgage Group, with no U.S. credit history or income verification required.

Q5: How many units are available and what are the price ranges?

A: Only 13 of the 26 total units remain, ranging from 570 to over 1,000 square feet. Prices start around $700,000 and go up to approximately $1.5 million.

Last week, we helped a Singapore billionaire extract $25M from his good class bungalow (GCB) valued at $35M in District 9, and the funds were used to acquire an overseas investment opportunity which needed to close in 3 weeks. The deal was referred to us by our private banking partner.

Over the past 2 years, we have funded nearly $500M in Singapore real estate alone!

Other fundings in April:

$5M loan - Grange Road apartment - funds used to acquire restaurants being sold below market value.

$7M loan - Claymore apartment - funds used to repatriate to an Indonesian company for working capital purposes.

$2M loan - District 10 semi-D - funds used for development financing on other Singapore real estate.

What is a Bridging Loan?

Bridging loans offer a short-term financing solution that uses only the value of the property as collateral and not your personal income and are used when speed and certainty of funding are the main priorities.

In Singapore, these loans are commonly used to release equity for business ventures, investment opportunities, or other immediate financial needs.

Unlike traditional loans, bridge loans are asset-backed, relying on the value of the borrower's property rather than their personal financials.

These loans typically feature "interest-only" or "interest-servicing only" payments, with a bullet repayment at the end of the term.

We offer bridging loans in: Singapore, the U.S., London, Australia and Thailand

Typical uses of funds also include:

GMG Bridging Loan Details:

Global Reach: Our Recent U.S. Bridge Loan Success

Our expertise is not limited to Singapore. We recently closed a $22M U.S. bridge loan in just 5 days, helping a global investor capitalize on a time-sensitive opportunity.

Read the full Press Release here.

Contact me directly!

Whether you're in Singapore or investing overseas, we can help you unlock fast, flexible funding through tailored bridging solutions. If you're working on a time-sensitive deal or just want to explore your options, I'm happy to walk you through it.

Email, WhatsApp, or schedule a call with me directly.

Your Top Questions Answered:

Q1: What exactly is a bridging loan and how does it work in Singapore?

A: A bridging loan is a short-term financing option that lets you unlock equity from your property quickly. It’s asset-backed, meaning approval is based on your property’s value, not your income.

Q2: How fast can Global Mortgage Group arrange a bridging loan?

A: GMG can approve loans within 48 hours, with funding typically completed in less than 30 days. If the property is unencumbered, funds can be released in as little as 7 days.

Q3: What can the funds from a bridging loan are used for?

A: Borrowers often use funds to seize urgent investment opportunities, acquire assets, pay down debt, or access working capital. It’s ideal for time-sensitive financial needs.

Q4: Are there any restrictions on who can apply for a bridging loan?

A: No, bridging loans have no age restrictions and don’t require income proof. The key eligibility factor is the property’s value, making it suitable for high-net-worth and asset-rich clients.

Q5: In which countries does Global Mortgage Group offer bridging loans?

A: GMG provides bridging loans in Singapore, the U.S., London, Australia, and Thailand, serving clients who need fast, flexible funding across global real estate markets.

Rising rates. Soaring tariffs. Global uncertainty.

Sounds like a time to sit on the sidelines, right? Not exactly.

For savvy investors, these are the signals of opportunity - especially in U.S. real estate.

We recently hosted an exclusive webinar with our Co-Founder, Donald Klip, where he unpacked what’s really happening beneath the headlines—and why current market conditions are creating a strong window of opportunity for foreign nationals and U.S. expats looking to invest in U.S. real estate.

A supply crisis hiding in plain sight

While much of the media focuses on Fed policy and mortgage rate spikes, a more powerful force is quietly driving the U.S. housing market: an unprecedented shortage of homes.

Estimates show the country is short by 5 to 7 million homes. Rising tariffs are also pushing up the cost of imported construction materials, from Canadian lumber to Chinese tools, which is slowing new developments even further.

With fewer homes being built and demand continuing to rise, the result is predictable: prices are holding steady and rental yields are climbing.

In fact, in 2022, despite the Fed raising interest rates from 0.25% to over 4.25%—the sharpest annual increase in four decades—U.S. home prices still rose by 10.2%, according to the Federal Housing Finance Agency (FHFA). That’s not just resilience; it’s a sign of a strong asset.

The “new” American dream and what it means for landlords

There was a time when the American Dream meant working hard, buying a home, and raising a family. However, with median home prices now 6–7 times the average household income, homeownership is no longer attainable for many Americans.

Instead, more people are renting, and that trend is accelerating. This is great news for landlords and rental investors. The shift from ownership to tenancy is driving up demand for well-located, investor-owned properties, particularly in migration hotspots.

For foreign investors, this presents an opportunity to enter markets where tenants are plentiful and rental income potential is strong. According to ATTOM’s Q1 2025 Single-Family Rental Market Report, gross rental yields across U.S. counties vary widely, with many affordable and emerging markets offering yields starting from 8% and reaching up to 18%.

These returns are significantly higher than those typically seen in many international property markets, making U.S. real estate a compelling option for global investors in 2025.

Migration is reshaping where investors are looking

Americans are on the move. Whether it’s to escape high costs, pursue better job opportunities, or benefit from lower taxes, more people are relocating, and doing so quickly.

States like Texas, Florida, Tennessee, Georgia, North and South Carolina are seeing a steady stream of new residents. Why? They offer strong job growth, particularly in industries like EVs, semiconductors, and logistics, along with no state income tax and relatively affordable housing.

For investors, this shift isn’t just interesting; it presents a clear opportunity. When people move, rental demand follows. These are the markets where growth is accelerating, infrastructure is expanding, and property values are poised to rise.

Why Buying Now Sets You Up for Future Equity

While some investors may hesitate in a high-rate environment, there are strong reasons why now may be exactly the right time to enter the market.

The logic is simple: lock in today’s pricing, refinance when rates drop.

When interest rates fall, and market indicators suggest that could happen soon, home prices are expected to jump. For investors who buy during the rate spike, this can lead to equity gains, refinancing opportunities, and the chance to pull cash out for their next investment.

Do I need U.S. credit to invest?

Absolutely not! If you’re a foreign national, you do not need U.S. credit to invest using America Mortgages’ market rate mortgage loans for investors. On top of that, the loans qualify on the property’s cash flow/rental on a 1:1 basis. No personal income taxes or end-of-year statements required. It’s common sense underwriting at its best!

Does a U.S. Expat need W2 income?

Absolutely not. If you’re a U.S. expat and you still maintain U.S. credit, you can qualify just as if you were living and working in the U.S. but with foreign-earned income allowed and no W2 required. A real game changer if you’ve tried other banks!

At America Mortgages, we approve clients based on the property’s projected rental income—not your personal income. If the rent covers the mortgage, you qualify.

Loan highlights:

This is how global investors are entering the U.S. market—easily, affordably, and with confidence.

Watch our recent webinar

If you missed it, watch the full webinar here.

Want to explore your options or get pre-approved?

Contact us today, and let’s walk you through a seamless mortgage journey.

Your Top Questions Answered

1. Is now a good time to invest in U.S. real estate?

Yes. Even during aggressive rate hikes, U.S. home prices rose over 10% in 2022. Limited supply and rising construction costs due to tariffs are keeping prices and yields strong. It’s a landlord’s market.

2. Should I wait for Fed rate cuts or buy now?

Don’t wait. Property prices tend to jump as soon as rates drop. Lock in today’s pricing, then refinance later for better terms and equity gains.

3. What’s the fastest way to get started?

Get pre-approved. America Mortgages can issue a pre-approval within 24 hours—no U.S. credit or tax returns required. We also help connect you with realtors in top U.S. investment cities.

4. How do migration trends affect investment strategy?

Migration drives demand. States like Texas, Florida, and the Carolinas are seeing population growth, job expansion, and rising rents. If people are moving there, investors should be too.

Read the full Q&A here.

Global Asset-Backed Bridging Loans

Tight credit conditions globally have created a vacuum in bank lending and when borrowers need to access cash quickly, there are limited ways to accomplish this.

We can help!

Access your home equity in the U.S., London, Australia and Singapore through a short-term loan called an Asset-backed bridging loan.

Bridging loan details:

In Singapore, these loans are not bound by TDSR since they are private loans. We have funded over $450M over the past 18 months, many of which are Good Class Bungalows, Shophouses, Landed, Condos and other high-value properties.

Typical Uses of Funds Include:

Our team of ex-bankers work with sophistication, discretion and care.

How Bridging Loans Work

Bridging loans are short-term loans, usually 1-2 years, used to bridge a funding gap where banks cannot meet borrower requirements such as speed of funding, loan-to-value (LTV), and certainty. These loans are asset-backed, relying on the collateral value of the property rather than the borrower's personal financials. They typically feature "interest-only" or "interest-servicing only" payments with a bullet repayment at the end of the term.

In a recent press release in Singapore, Global Mortgage Group set a new benchmark in a record-breaking month by facilitating bridge loans for two high-end condominiums, three bungalows, and one Good Class Bungalow (GCB). In 2024, GMG has funded over $186 million in bridging loans in Singapore alone.

Examples of how we helped our clients

USA

An SE Asian office owned 3 homes in California free and clear, worth $17M. Since the homes were empty and used as second homes, bank financing was not an option, and the client needed funding within a month to be repatriated back home for working capital. We secured an interest-only $10M loan for 2 years, funded in 2 weeks!

England

A private bank referred a client who needed to purchase a Golden Visa in Europe. However, since their country had capital controls, they were not able to move the required amount of funds in the necessary time frame. We secured a bridging loan against their U.K. prime real estate to be used for the Golden Visa investment. The terms were 1 year, 70% LTV, and funded in 3 weeks!

Singapore

Our client, a Singaporean entrepreneur, owns a $15 million landed property. To expand his retail business, he secured a $11.25 million bridge loan (75% LTV) over 12 months. This provided liquidity to complete his shophouse purchase without selling his bungalow, funded in 3 weeks!

Global Affiliate Program

If you have any friends or clients that require any global real estate financing, we pay a generous referral fee for any successful funding. Message me to learn more.

Your Top Questions Answered:

Q1: What is an asset backed bridging loan offered by Global Mortgage Group?

A: An asset backed bridging loan is a short term funding solution secured by property value, helping clients access cash quickly when traditional banks cannot lend.

Q2: Who is eligible to apply for a bridging loan?

A: Anyone owning property in the US, UK, Singapore, or Australia can qualify based solely on property value without income proof, age limit, or residency requirements.

Q3: How fast can I receive funding through Global Mortgage Group?

A: Approvals are typically issued within 48 hours, and funds can be disbursed in under 30 days or even within 7 days for debt free properties.

Q4: What can the funds from a bridging loan are used for?

A: Funds can be used for buying property, Golden Visas, investments, tuition, healthcare, or paying down high cost debt for any legitimate financial need.

Q5: How does Global Mortgage Group support clients during the loan process?

A: Our team of experienced bankers manages every step with confidentiality and efficiency, ensuring smooth and fast funding tailored to each client’s goals.

Quick housekeeping: My interview with Max Chernov has reached 350,000 views. Check it out if you haven’t, where I talk about global real estate investing and financing. Lastly, please follow me on my new Instagram page @theglobalmortgageguy.

Please scroll down for Upcoming speaking events in Singapore and on our various YouTube channels.

Let’s start.

In my past life, I started one of the first hedge funds in Hong Kong and subsequently ran global hedge fund coverage desks for some of the top investment banks - in fact, my exact role was Harper Stern's, and eventually her boss Eric's job in the HBO Series, Industry.

Soros was one of my clients and Scott Bessent specialized in geopolitics and macro - my area of focus. I was the "China Guy" for many global hedge funds as China was the biggest theme globally, especially when it entered the WTO in 2001.

Scott and the folks at Soros (and other hedge funds) in the 2000s were some of the brightest minds in the world - he certainly knows what he's doing, and bringing in a market participant to manage the current environment is a smart move.

In this week's Bloomberg Interview, Scott talked about the need to bring down the entire yield curve, particularly the 10-year as it relates to the cost of funding (mortgage rates) and monetizing the asset side of the government's balance sheet.

A few weeks into the job, and here are my takeaways:

1. He criticized Janet Yellen for not "terming out" existing debt but then continued the same monetary policy. That tells me that there are no alternative options currently (Scylla and Charybdis).

2. DOGE is an incredible and long-overdue initiative. The U.S. simply spends too much.

However, -> the amount saved is still not enough to affect the deficit meaningfully.

Taken from Luke Gromen’s FFTT February 7th, 2025 => ”To frame this properly: Assuming $5T in Federal receipts this year (flat) and the annualized spending above, the U.S. could cut DoD spending by 100%, as well as cut all other Federal spending by 100%...and the U.S. would STILL run a $140B deficit. “DOGE” is gonna need a bigger boat.”

3. Any and all “out of the box” ideas are going to get attention - starting with the one below…

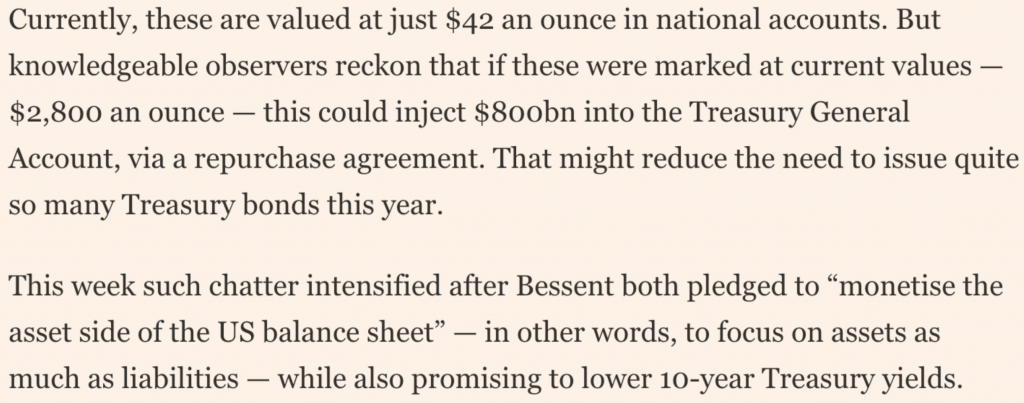

4. The Fed may revalue their Gold holdings at $42/oz (not a typo!) to the current market price of $2800/oz immediately adding nearly $1TN to the Treasury’s General Account. Read this fantastic FT Article from Sunday by Gillian Tett!

Here is the FT excerpt:

=> This would lessen the need to issue longer term debt which will have the same effect as QE.

The big ticket items on the Annual Federal Budget

Luke argues that the only thing that can be reduced is Gross Interest Expenses which relies on a much lower 10-year bond yield.

If we get $500BN in savings from DOGE + $1TN revalue from Gold, and cut interest expenses to $800BN = then we are back in the game!

=> I think they have no choice but to engineer this to happen. There may be some short-term pain, mostly from equities, but imagine a world where mortgage rates are 3-4%.

Similar to 2019, the market priced in 2 rate cuts and we ended the year with 4 - NO ONE is expecting rates to fall this much!

=> I think 10-year yields could end the year at 4-5%, falling to 3-4% in 2026

=> Needless to say, this is very bullish for U.S. home prices.

Upcoming Events (DM me if interested):

Q1: What insights did Scott Bessent share about managing the current economic environment?

A: Scott Bessent emphasized the need to lower the entire yield curve and strategically monetize government assets to reduce funding costs, influencing both mortgage rates and fiscal policy.

Q2: How could gold revaluation affect the U.S. Treasury and housing market?

A: By adjusting gold holdings from $42/oz to market value, the Treasury could gain nearly $1 trillion, easing debt issuance pressures and potentially lowering mortgage rates, benefiting homeowners.

Q3: What role does Global Mortgage Group play in understanding these financial strategies?

A: Global Mortgage Group provides analysis and insights on macroeconomic trends, real estate investing, and mortgage strategies, helping investors and homebuyers navigate changes in interest rates and fiscal policy.

Q4: Are lower mortgage rates expected soon and what could drive them?

A: Market signals suggest 10-year yields could fall to 3-4% by 2026, driven by gold monetization, savings from federal spending, and interest expense reductions, which could make U.S. home loans more affordable.

Q5: Where can I access more interviews and discussions on real estate and global finance?

A: You can watch interviews and panels on Global Mortgage Group’s YouTube channel, check out the Real Asia Show, and follow @theglobalmortgageguy on Instagram for updates and upcoming speaking events.

Trade war has begun

Trump has implemented 25% import tariffs from Mexico and Canada and 10% on Chinese imports. Honestly, there is no way to know the outcome, but one thing for sure is that commodity and asset prices will be volatile as we price in the "Tariff Uncertainty".

Interestingly, all of Canada's $200B trade surplus with the U.S. comes from oil coming from Alberta. This heavy-grade crude is mixed with U.S. crude and refined. I read that if you strip out oil, there would be no trade surplus.

Tariff Economics

Tariffs are initially paid by importers, but who ultimately absorbs the cost depends on how easily they can find alternative suppliers.

If alternatives are readily available, suppliers may lower their prices, minimizing the impact on importers.

However, if finding substitutes is difficult, suppliers have little incentive to reduce costs, forcing importers to absorb the tariff burden.

During the tariff increases of 2018 and 2019, U.S. importers struggled to secure alternative suppliers, leading them to bear most of the costs (lower margins).

In the short term, businesses reliant on affected imports face higher production expenses and must decide whether to pass these costs onto consumers or absorb them by reducing profit margins.

=> Trump Angle: If corporate taxes are lowered I'm the U.S. (being discussed), companies will have some financial wiggle room to absorb any cost increases from higher tariffs.

DeepSeek

This is disruptive (on the surface) to AI as it appears to require less computing power (less GPUs) to achieve the same outcome, and clearly, the market will need to rethink its forecasts across the entire AI vertical. This "increases" the need for NVDA chips as more players will be able to get into the space with less capital. This will lead to a faster commoditised AI-information world (Singularity).

AI is currently in the training phase, which means we are only at the stage of AI that takes data - known as Large Language Models (LLM) - and "trains" it to answer questions – mostly search-related. The next stage of AI is the Inference Phase, which makes conclusions and decisions – not there yet, but not far away.

To me, AI is like a fast food restaurant. Each company has the same ingredients, but each is trying different sequences to create the fastest, cheapest and most delicious burger. McDonalds can put ketchup on the bread before the lettuce, and Burger King may put pickles before the ketchup, then patty before lettuce, etc.

This is what DeepSeek has done.

OpenAI used the sequence of both "Supervised Fine-tuning" then "Reinforcement Learning".

What DeepSeek did was take various sources of data but eventually only used "Reinforcement Learning" to skip steps (and lower costs).

Another misconception is "Open Code" and "Open Sourced".

DeepSeek is an Open Code, which means they publish a whitepaper and show models and model weights, BUT they DO NOT show the data, so it's not actually Open Sourced.

There has been a big selloff across the AI vertical - Software, LLM, chips and Nuclear are all being sold off. While the timing of this is peculiar, with the origins of DeepSeek being from a quant hedge fund, you can't ignore its implications.

I personally think it's too early to bottom-fish, given there are clearly some geo-political issues here, and the market will be focused on the trade wars happening, and chips will be a sensitive topic.

Rates

Fed unchanged, and long-term yields did not move during the FOMC meeting.

The 10-year moved up a little on the tariff announcement, and we saw some lenders raise mortgage rates, but we lowered our rates slightly last week. Honestly, I am surprised at the inactivity of the bond market – I suspect yields were kept under wraps with some AI selloff flow moving into bonds.

It will take a while to see how the tariffs will affect the economy, prices, and rates, but if we look at what happened in 2019, rates moved lower despite the trade war.

This time around is more serious, but the bottom line is rates are determined by inflation and growth expectations, to name a few – that is where we need to focus on.

On the other hand, after the Smoot Hawley Act in 1930, the last across-the-board tariff increases, the stock market suffered major losses, and the economy went into a deep recession.

My big bet on a weaker USD has not transpired yet which is the main wildcard for any growth to happen in the U.S. We need a weaker USD.

The Real Asia Show

Finally, I have started a YouTube channel called The Real Asia Show, where I interview interesting people across Asia on their journey to where they are now, the challenges they faced, and things they can teach us. Hopefully, there are some meaningful takeaways. Please subscribe.

I have also launched 2 Instagram channels:

Happy Hunting!

Donald Klip, Co-Founder

Global Mortgage Group

Mobile: +65 9773-0273

Email: [email protected]

Q1: How do tariffs impact mortgage rates in the U.S.?

A: Tariffs increase import costs, which can affect inflation and economic growth. While some lenders may raise mortgage rates in response, Global Mortgage Group monitors these changes to help borrowers find the best opportunities.

Q2: What is DeepSeek and why is it important for the AI industry?

A: DeepSeek is a disruptive AI approach that reduces computational costs by using reinforcement learning instead of traditional multi-step training. This innovation could accelerate AI development and reshape the market.

Q3: How have past trade wars influenced the economy and interest rates?

A: Historical trade conflicts, like the 2018-2019 tariff increases, caused volatility in asset prices. Mortgage rates initially rose but later fell, showing that trade tensions can affect both markets and borrowing costs over time.

Q4: What can viewers expect from The Real Asia Show?

A: The Real Asia Show features interviews with influential figures across Asia, sharing insights on business, investing, and personal growth. It’s a resource for learning practical lessons from real-world experiences.

Q5: Where can I follow updates from Global Mortgage Group on tariffs and real estate trends?

A: You can follow Global Mortgage Group on YouTube via The Real Asia Show, and on Instagram through The Global Mortgage Guy and Real Estate Investing 101 for the latest insights on mortgage rates and investing strategies.

Global Mortgage Group Pte. Ltd. is an international real estate finance firm specialising in high net worth mortgages, equity release, bridging loans, and private credit across 23+ markets. Based in Singapore with offices and partnerships across the globe, we connect our international clients to our network of lenders around the world. GMG offers financing solutions in the United States, Canada, Latin America, United Kingdom, Europe, Middle East, and Asia-Pacific.